ING Direct – Let the Buyer Beware

Here is a my very unpleasant experience with ING Direct.

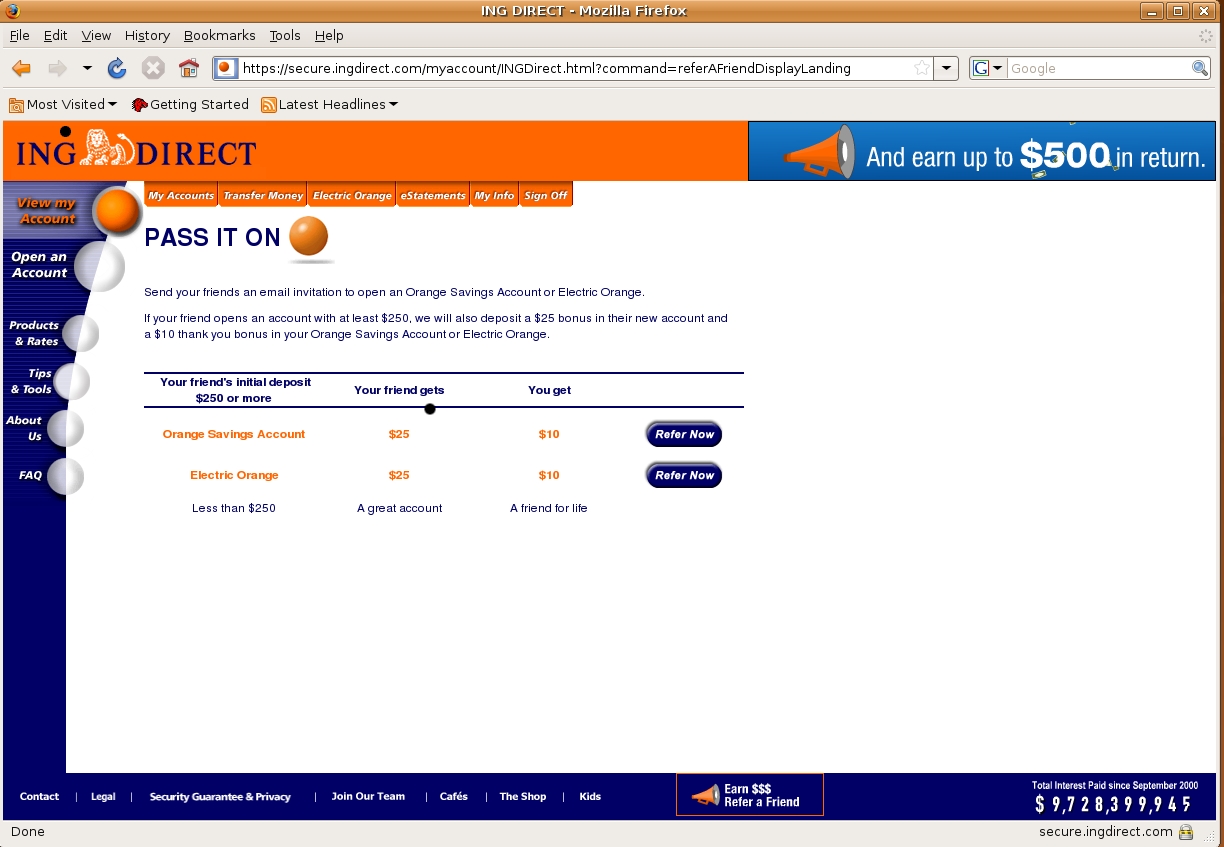

ING Direct, a U.S. branch of ING Group based in the Netherlands, advertises on its web site, http://farm4.static.flickr.com/3040/2904282333_d9550a396c_o.jpg, if a customer refers a friend to open an “Orange Savings Account” or an “Electric Orange” account with $250 or more, the friend would get $25 and the existing customer would get $10.

I referred someone to open an account at ING Direct but never received my $10. It is not the $10 that caused me to post this blog, it is the principle and the false advertisement on ING Direct part.

Here is the story:

When the referree got the invitation from me, she was ready to open an account. But the disclosure statement about the Savings Account mentions terms pertaining to an Orange CD account. Concerned that her money might actually end up in a CD, she called ING Direct. The ING agent told her the Orange Savings Account is not a CD and assured her her funds would be liquid. The ING agent proceeded to tell her that an Orange CD account pays at a higher interest rate. When tasked about the $25 bonus, the agent told the referree she wouldn’t get the $25 bonus unless she opens an Orange Savings Account. That was fine and dandy. But the agent continued to tell the referree she should open an Orange CD right away to lock in the interest rate and could open an Orange Savings Account afterwards and still get the bonus. She did.

She opened an Orange CD to lock in the interest rate and then tried to open an Orange savings account later that same day but could not. Another phone call ended with the assurance that only one account can be opened a day and that she should open the Savings after the CD is assured. In the meantime, she was assured there would be no problem about the bonuses if the agent gave the incorrect information as the research department would go over the phone calls to make the determination.

A few days later after the CD was established, the referree called back to open the Savings account and was given the $25 credit instantly but was told I had to call to receive my $10.

When I made the call, another ING Direct agent said the referree was not entitled to the $25 and I was I not entitled to the $10 bonus because she was an existing customer when she opened the Orange Savings Account. The agent threatened to remove the $25 from her account at which point the referree asked to speak to a supervisor and was transferred to Mark, the floor manager, employee #702144, located in Delaware. Mark was rude on the phone and asked many unnecessary personal questions. Those questions had nothing to do with $10 bonus and ING policy. I decided it’s not worth dealing with him or ING Direct anymore. I will be closing my account with them as soon as interest is posted this month.

Wednesday, September 24, 2008

{kind=link}

Candidates' tax plan

http://www.webcpa.com/article.cfm?ARTICLEID=29350

Both Candidates' Plans Would Reduce Tax Liabilities

Washington, D.C. (Sept. 24, 2008)

By WebCPA staff

A study of both presidential candidates' tax plans finds that they will both reduce millions of taxpayers' liability to zero.

According to Internal Revenue Service statistics for 2006, 45.6 million tax filers, or about one-third of all filers, have no tax liability after taking credits and deductions. "For good or ill, this is a 57 percent increase since 2000 in the number of Americans who pay no personal income taxes," wrote Scott A. Hodge, in a study for the Tax Foundation. He estimates that there will be 47 million tax returns with zero income tax liability in 2009 under current law.

The foundation's estimates show that if all of the tax provisions proposed by Sen. Barack Obama, D-Ill, are adopted next year, the number of non-payers would rise by approximately 16 million, to a total of 63 million, or about 44 percent of all tax filers. If all the tax proposals of Sen. John McCain, R-Ariz., were enacted in 2009, the number of taxpayers with zero tax liability would increase a million less, by about 15 million to 62 million overall, or about 42 percent of all tax filers.

The Obama tax plan contains seven new tax provisions, including a Making Work Pay Credit, a Universal Mortgage Credit, and a plan to eliminate income taxes for seniors earning under $50,000, while McCain's health care credit offers incentives for people to buy their own health insurance.

"This tax provision has a bigger impact on cutting people's taxes than any single proposal from either party," wrote Hodge. "Obama uses a longer list of smaller tax credit ideas to reduce a similar number of taxpayers' liability to zero."

___

Here is a Wall Street Journal article on the two presidential candidates' tax plan:

http://online.wsj.com/article/SB122221857642269749.html

The article provided a couple of external links with overview of the two plans:

Grant Thornton has an overview chart.

Deloitte & Touche provides a detailed 14 page summary.

And here is the same WSJ article on Yahoo, http://biz.yahoo.com/wallstreet/080924/sb122221857642269749_id.html.

A friend, Jerry Gropp AIA, from Mercer Island sent me this link, which is excellent:

https://knol.google.com/k/jeffrey-gramlich/the-mccain-and-obama-tax-plans-for/2k7f943jjgete/3#

Both Candidates' Plans Would Reduce Tax Liabilities

Washington, D.C. (Sept. 24, 2008)

By WebCPA staff

A study of both presidential candidates' tax plans finds that they will both reduce millions of taxpayers' liability to zero.

According to Internal Revenue Service statistics for 2006, 45.6 million tax filers, or about one-third of all filers, have no tax liability after taking credits and deductions. "For good or ill, this is a 57 percent increase since 2000 in the number of Americans who pay no personal income taxes," wrote Scott A. Hodge, in a study for the Tax Foundation. He estimates that there will be 47 million tax returns with zero income tax liability in 2009 under current law.

The foundation's estimates show that if all of the tax provisions proposed by Sen. Barack Obama, D-Ill, are adopted next year, the number of non-payers would rise by approximately 16 million, to a total of 63 million, or about 44 percent of all tax filers. If all the tax proposals of Sen. John McCain, R-Ariz., were enacted in 2009, the number of taxpayers with zero tax liability would increase a million less, by about 15 million to 62 million overall, or about 42 percent of all tax filers.

The Obama tax plan contains seven new tax provisions, including a Making Work Pay Credit, a Universal Mortgage Credit, and a plan to eliminate income taxes for seniors earning under $50,000, while McCain's health care credit offers incentives for people to buy their own health insurance.

"This tax provision has a bigger impact on cutting people's taxes than any single proposal from either party," wrote Hodge. "Obama uses a longer list of smaller tax credit ideas to reduce a similar number of taxpayers' liability to zero."

___

Here is a Wall Street Journal article on the two presidential candidates' tax plan:

http://online.wsj.com/article/SB122221857642269749.html

The article provided a couple of external links with overview of the two plans:

Grant Thornton has an overview chart.

Deloitte & Touche provides a detailed 14 page summary.

And here is the same WSJ article on Yahoo, http://biz.yahoo.com/wallstreet/080924/sb122221857642269749_id.html.

A friend, Jerry Gropp AIA, from Mercer Island sent me this link, which is excellent:

https://knol.google.com/k/jeffrey-gramlich/the-mccain-and-obama-tax-plans-for/2k7f943jjgete/3#

Tuesday, September 23, 2008

Tax Provisions in CA Budget

Here is a list of tax-related changes. Provisions that are different or not contained in the original set of budget bills say New.

▸ The LLC fee is accelerated, and calendar-year LLCs must pay their 2008 fee on April 15, 2009, and estimated 2009 fee on June 15, 2009.

▸ Business credits are limited to 50% of tax liability for 2008 and 2009, with an exception for small businesses.

▸ The 12-month rule for use tax on vehicles, vessels, and aircraft purchased outside of California is back, effective the date of enactment.

▸ The NOL deduction is suspended for 2008 and 2009, with an exception for small businesses. However, for taxable years beginning on or after January 1, 2008, NOLs may be carried forward for 20 years; NOLs may be carried back for two years for losses generated in taxable years beginning on or after January 1, 2011.

▸ New For taxable years beginning on or after July 1, 2008, affiliated corporations may share credits.

▸ Beginning January 1, 2009, the first two estimated payments for individuals and corporations are increased from 25% to 30%, and the last two are reduced to 20%.

▸ Individual taxpayers with income over $1 million may no longer use the 110% of prior-year tax as a safe harbor for years beginning in 2009.

▸ New The 1% mental health surcharge will be imposed on California-source taxable income for any electing nonresident partner or director of a corporation included in a group return if the total income is in excess of $1 million.

▸ New There will be a new corporate penalty equal to 20% of an understatement of tax for corporations with understated tax of more than $1 million.

▸ New Certain individuals are required to make tax payments electronically for payments made on or after January 1, 2009.

(Source: http://www.caltax.com/Flash%20E-Mail/Pages/Newbudgetsigned.aspx)

▸ The LLC fee is accelerated, and calendar-year LLCs must pay their 2008 fee on April 15, 2009, and estimated 2009 fee on June 15, 2009.

▸ Business credits are limited to 50% of tax liability for 2008 and 2009, with an exception for small businesses.

▸ The 12-month rule for use tax on vehicles, vessels, and aircraft purchased outside of California is back, effective the date of enactment.

▸ The NOL deduction is suspended for 2008 and 2009, with an exception for small businesses. However, for taxable years beginning on or after January 1, 2008, NOLs may be carried forward for 20 years; NOLs may be carried back for two years for losses generated in taxable years beginning on or after January 1, 2011.

▸ New For taxable years beginning on or after July 1, 2008, affiliated corporations may share credits.

▸ Beginning January 1, 2009, the first two estimated payments for individuals and corporations are increased from 25% to 30%, and the last two are reduced to 20%.

▸ Individual taxpayers with income over $1 million may no longer use the 110% of prior-year tax as a safe harbor for years beginning in 2009.

▸ New The 1% mental health surcharge will be imposed on California-source taxable income for any electing nonresident partner or director of a corporation included in a group return if the total income is in excess of $1 million.

▸ New There will be a new corporate penalty equal to 20% of an understatement of tax for corporations with understated tax of more than $1 million.

▸ New Certain individuals are required to make tax payments electronically for payments made on or after January 1, 2009.

(Source: http://www.caltax.com/Flash%20E-Mail/Pages/Newbudgetsigned.aspx)

Monday, September 22, 2008

"First-time" Home Buyer Credits

The IRS has provided certain guidance on the so called "first-time" home buyer tax credit, see http://www.irs.gov/newsroom/article/0,,id=186831,00.html.

Thursday, September 18, 2008

Record Retention

I often get inquiries on how long records should be kept. My normal answer is to keep tax returns, general ledgers, & financial statements permanently and supporting documents such as cancelled checks, paid invoices, billings, check registers, etc. for 7 years. Remember supporting documents on purchases of real estates, stocks, bonds, etc. should be kept for 7 years beyond the date the underlying assets are sold.

Here is link which includes additional information. While that site recommends a shorter period of some records, there may be other reasons for keeping some records a bit longer.

The IRS also has a page on recommended record retention, http://www.irs.gov/businesses/small/article/0,,id=98513,00.html. But my recommendation is to use the IRS recommendation as a reference only.

Here is link which includes additional information. While that site recommends a shorter period of some records, there may be other reasons for keeping some records a bit longer.

The IRS also has a page on recommended record retention, http://www.irs.gov/businesses/small/article/0,,id=98513,00.html. But my recommendation is to use the IRS recommendation as a reference only.

Estimated 2009 Tax Brackets

http://www.webcpa.com/article.cfm?articleid=29182&pg=ros

Analysts Forecast 2009 Tax Brackets and Deductions

New York (Sept. 18, 2008)

By WebCPA staff

CCH and Thomson Reuters' RIA unit have calculated the inflation-adjusted amounts for tax brackets, standard deductions and exemptions for next tax season.

RIA predicts that the basic standard deduction for 2009 for joint returns and surviving spouses will be $11,400, up from $10,900 in 2008. For single taxpayers, RIA forecasts the standard deduction will be $5,700, up from $5,450 in 2008. For head of household, the amount will be $8,350, up from $8,000.

CCH predicts that a married couple filing jointly with total taxable income of $100,000 will pay $312.50 less in income taxes in 2009 compared to 2008. A single filer with taxable income of $50,000 will save $156.25 next year.

CCH predicted that single taxpayers and married taxpayers filing separately could see a $250 increase over 2008 in their standard deduction, to $5,700, while the standard deduction for joint filers will increase by $500 to $11,400. Heads of households will see an increase in their standard deduction of $350, to $8,350.

The additional standard deduction for those age 65 or older or who are blind, will rise $50 to $1,100 in 2009 for married individuals and surviving spouses, and $50 to $1,400 for single filers. The personal exemption amount will go up in 2009 by $150 to $3,650.

For an individual who can be claimed as a dependent on another's return, RIA predicts that the basic standard deduction for 2009 will be $950, up from $900 in 2008, or $300 (same as in 2008), plus the individual's earned income, whichever is greater. For 2009, the additional standard deduction for married taxpayers 65 or over or blind will be $1,100, up from $1,050 in 2008. For a single taxpayer or head of household who is 65 or over or blind, the additional standard deduction for 2009 will be $1,400, up from $1,350 in 2008.

The personal exemption amount for 2009 will rise to $3,650, up from $3,500 in 2008, according to RIA. The exemption from the kiddie tax for 2009 will be $1,900, up from $1,800 in 2008. A parent will be able to elect to include a child's income on the parent's return for 2009 if the child's income is more than $950 and less than $9,500, up from $900 and $9,000 in 2008. For 2009, CCH predicts the kiddie tax standard deduction will rise to $950.

CCH's projected tax brackets are available here.

RIA's projected tax brackets are below:

FOR MARRIED INDIVIDUALS FILING JOINT RETURNS AND SURVIVING SPOUSES, THE 2009 RATE BRACKETS ARE:

Not over $16,700 - 10% of taxable income

Over $16,700 but not over $67,900 - $1,670.00 plus 15% of the excess over $16,700

Over $67,900 but not over $137,050 - $9,350.00 plus 25% of the excess over $67,900

Over $137,050 but not over $208,850 - $26,637.50 plus 28% of the excess over $137,050

Over $208,850 but not over $372,950 - $46,741.50 plus 33% of the excess over $208,850

Over $372,950 $100,894.50 plus 35% of the excess over $372,950

FOR SINGLE INDIVIDUALS (OTHER THAN HEADS OF HOUSEHOLDS AND SURVIVING SPOUSES), THE 2009 RATE BRACKETS ARE:

Not over $8,350 - 10% of taxable income

Over $8,350 but not over $33,950 - $835.00 plus 15% of the excess over $8,350

Over $33,950 but not over $82,250 - $4,675.00 plus 25% of the excess over $33,950

Over $82,250 but not over $171,550 - $16,750.00 plus 28% of the excess over $82,250

Over $171,550 but not over $372,950 - $41,754.00 plus 33% of the excess over $171,550

Over $372,950 $108,216.00 plus 35% of the excess over $372,950

FOR HEADS OF HOUSEHOLDS, THE 2009 RATE BRACKETS ARE:

Not over $11,950 - 10% of taxable income

Over $11,950 but not over $45,500 - $1,195.00 plus 15% of the excess over $11,950

Over $45,500 but not over $117,450 - $6,227.50 plus 25% of the excess over $45,500

Over $117,450 but not over $190,200 - $24,215.00 plus 28% of the excess over $117,450

Over $190,200 but not over $372,950 - $44,585.00 plus 33% of the excess over $190,200

Over $372,950 $104,892.50 plus 35% of the excess over $372,950

FOR MARRIEDS FILING SEPARATE RETURNS, THE 2009 RATE BRACKETS ARE:

Not over $8,350 - 10% of taxable income

Over $8,350 but not over $33,950 - $835.00 plus 15% of the excess over $8,350

Over $33,950 but not over $68,525 - $4,675.00 plus 25% of the excess over $33,950

Over $68,525 but not over $104,425 - $13,318.75 plus 28% of the excess over $68,525

Over $104,425 but not over $186,475 - $23,370.75 plus 33% of the excess over $104,425

Over $186,475 $50,447.25 plus 35% of the excess over $186,475

FOR ESTATES AND TRUSTS, THE 2009 RATE BRACKETS ARE:

Not over $2,300 15% of taxable income

Over $2,300 but not over $5,350 - $345.00 plus 25% of the excess over $2,300

Over $5,350 but not over $8,200 - $1,107.50 plus 28% of the excess over $5,350

Over $8,200 but not over $11,150 - $1,905.50 plus 33% of the excess over $8,200

Over $11,150 - $2,879.00 plus 35% of the excess over $11,150

For subscribers of the Wall Street Journal, here is an article on the same subject:

http://online.wsj.com/article/SB122161922104346467.html

Analysts Forecast 2009 Tax Brackets and Deductions

New York (Sept. 18, 2008)

By WebCPA staff

CCH and Thomson Reuters' RIA unit have calculated the inflation-adjusted amounts for tax brackets, standard deductions and exemptions for next tax season.

RIA predicts that the basic standard deduction for 2009 for joint returns and surviving spouses will be $11,400, up from $10,900 in 2008. For single taxpayers, RIA forecasts the standard deduction will be $5,700, up from $5,450 in 2008. For head of household, the amount will be $8,350, up from $8,000.

CCH predicts that a married couple filing jointly with total taxable income of $100,000 will pay $312.50 less in income taxes in 2009 compared to 2008. A single filer with taxable income of $50,000 will save $156.25 next year.

CCH predicted that single taxpayers and married taxpayers filing separately could see a $250 increase over 2008 in their standard deduction, to $5,700, while the standard deduction for joint filers will increase by $500 to $11,400. Heads of households will see an increase in their standard deduction of $350, to $8,350.

The additional standard deduction for those age 65 or older or who are blind, will rise $50 to $1,100 in 2009 for married individuals and surviving spouses, and $50 to $1,400 for single filers. The personal exemption amount will go up in 2009 by $150 to $3,650.

For an individual who can be claimed as a dependent on another's return, RIA predicts that the basic standard deduction for 2009 will be $950, up from $900 in 2008, or $300 (same as in 2008), plus the individual's earned income, whichever is greater. For 2009, the additional standard deduction for married taxpayers 65 or over or blind will be $1,100, up from $1,050 in 2008. For a single taxpayer or head of household who is 65 or over or blind, the additional standard deduction for 2009 will be $1,400, up from $1,350 in 2008.

The personal exemption amount for 2009 will rise to $3,650, up from $3,500 in 2008, according to RIA. The exemption from the kiddie tax for 2009 will be $1,900, up from $1,800 in 2008. A parent will be able to elect to include a child's income on the parent's return for 2009 if the child's income is more than $950 and less than $9,500, up from $900 and $9,000 in 2008. For 2009, CCH predicts the kiddie tax standard deduction will rise to $950.

CCH's projected tax brackets are available here.

RIA's projected tax brackets are below:

FOR MARRIED INDIVIDUALS FILING JOINT RETURNS AND SURVIVING SPOUSES, THE 2009 RATE BRACKETS ARE:

Not over $16,700 - 10% of taxable income

Over $16,700 but not over $67,900 - $1,670.00 plus 15% of the excess over $16,700

Over $67,900 but not over $137,050 - $9,350.00 plus 25% of the excess over $67,900

Over $137,050 but not over $208,850 - $26,637.50 plus 28% of the excess over $137,050

Over $208,850 but not over $372,950 - $46,741.50 plus 33% of the excess over $208,850

Over $372,950 $100,894.50 plus 35% of the excess over $372,950

FOR SINGLE INDIVIDUALS (OTHER THAN HEADS OF HOUSEHOLDS AND SURVIVING SPOUSES), THE 2009 RATE BRACKETS ARE:

Not over $8,350 - 10% of taxable income

Over $8,350 but not over $33,950 - $835.00 plus 15% of the excess over $8,350

Over $33,950 but not over $82,250 - $4,675.00 plus 25% of the excess over $33,950

Over $82,250 but not over $171,550 - $16,750.00 plus 28% of the excess over $82,250

Over $171,550 but not over $372,950 - $41,754.00 plus 33% of the excess over $171,550

Over $372,950 $108,216.00 plus 35% of the excess over $372,950

FOR HEADS OF HOUSEHOLDS, THE 2009 RATE BRACKETS ARE:

Not over $11,950 - 10% of taxable income

Over $11,950 but not over $45,500 - $1,195.00 plus 15% of the excess over $11,950

Over $45,500 but not over $117,450 - $6,227.50 plus 25% of the excess over $45,500

Over $117,450 but not over $190,200 - $24,215.00 plus 28% of the excess over $117,450

Over $190,200 but not over $372,950 - $44,585.00 plus 33% of the excess over $190,200

Over $372,950 $104,892.50 plus 35% of the excess over $372,950

FOR MARRIEDS FILING SEPARATE RETURNS, THE 2009 RATE BRACKETS ARE:

Not over $8,350 - 10% of taxable income

Over $8,350 but not over $33,950 - $835.00 plus 15% of the excess over $8,350

Over $33,950 but not over $68,525 - $4,675.00 plus 25% of the excess over $33,950

Over $68,525 but not over $104,425 - $13,318.75 plus 28% of the excess over $68,525

Over $104,425 but not over $186,475 - $23,370.75 plus 33% of the excess over $104,425

Over $186,475 $50,447.25 plus 35% of the excess over $186,475

FOR ESTATES AND TRUSTS, THE 2009 RATE BRACKETS ARE:

Not over $2,300 15% of taxable income

Over $2,300 but not over $5,350 - $345.00 plus 25% of the excess over $2,300

Over $5,350 but not over $8,200 - $1,107.50 plus 28% of the excess over $5,350

Over $8,200 but not over $11,150 - $1,905.50 plus 33% of the excess over $8,200

Over $11,150 - $2,879.00 plus 35% of the excess over $11,150

For subscribers of the Wall Street Journal, here is an article on the same subject:

http://online.wsj.com/article/SB122161922104346467.html

Subscribe to:

Posts (Atom)